When a nation starts to descend into a crisis, the satire and ironic humour of its hapless citizenry begins to blossom. India is at that stage. Quiz questions like “What will hit Rs 100 first, a kg of onions, the dollar or a litre of petrol?” and funnies like “Nowadays, Indian exporters meet at Vivanta and importers at Sukh Sagar” and “If money is the root of all evil, then the rupee is the square root” are doing the rounds in Mumbai, our financial centre. On social media, adverts for engagement rings have replaced diamonds with onions, and jokes abound about the onion being a monetary unit larger than a trillion, and the rupee being replaced by the onion as legal tender.

The desperation of the citizenry is clearly lost on the policymakers in Delhi, whose every action is intensifying the country’s financial misery and dark humour. The economic mismanagement of the past four years has been exacerbated in the last month by the raising of short-term interest rates, the bond market sell-off, mounting debts absorbed by the public sector banks, the food security bill, capital controls, gold import restrictions and the absurd taxes on imported television sets, among other actions.

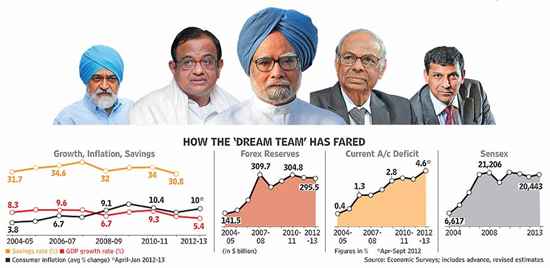

Can this be reversed? Not if the so-called ‘dream team’ at the helm of India’s economics continues in its misplaced labours. The team currently comprises Prime Minister Manmohan Singh, Montek Singh Ahluwalia of the Planning Commission, Finance Minister P. Chidambaram, Economic Advisor and former RBI Governor C. Rangarajan and the new RBI Governor and IMF economist Raghuram Rajan. While Manmohan Singh and Chidambaram have a record of reform, that is firmly in the past, and their good habits have not carried over into the present. Over the past decade, none of the current caretakers of India’s economy have a landmark reform marked to their name; in the last year, this condition has become especially acute as the economic crisis has deepened.

What has gone wrong? Cynically putting politics and electoral logic ahead of the economy and prosperity, and slavish obedience to political masters, for sure. But also plain poor leadership—and survival through a round robin of blame. The Planning Commission chair blames the finance minister, who faults the U.S. Federal Reserve and our own Reserve Bank, which cites the limitations of its mandate, and looks to the prime minister who speaks so softly that he is inaudible even to his economic advisors whose counsel is contrary to their own previously proffered knowledge.

For after Manmohan Singh, the public’s deepest disappointment is reserved for Raghuram Rajan, the renowned economist imported from the IMF and the University of Chicago barely a year ago precisely for his bold views. Indeed, in the 2012-2013 Economic Survey of India which he authored, he recommended curbing the 5 per cent fiscal deficit by ending wasteful subsidies, structural reform and job creation, lowering interest rates, controlling inflation and decried capital controls. Instead, he has acquiesced to the opposite of all the above, including passing the damaging Food Security Bill. Despite living and working in a liberal economy like the U.S. for 25 years, despite boldly predicting the global financial crisis, despite his sound economic principles, he has chosen not to dissent while in New Delhi. He is now party to the collapse of a once robust emerging market with much hope for its youthful population—surely a blemish on his own once-promising intellect.

The Mumbai share bazaar, which was already sent to hell by the coalition partners of the 2004 UPA dream team’s government but to whose doors the 2009 UPA government has begged foreign institutional investors to recongregate, has expressed its disenchantment with dramatic daily sell-offs. In its lexicon, the term ‘dream team’ has been replaced by the ‘Nightmare from Delhi’. The market gives the dream team 0/10—indeed, it gets negative marks.

There’s little to do now for the rest of us, but to:

- Hope that the U.S. employment numbers stall and so does its recent manufacturing revival so that the U.S. Federal Reserve can continue its quantitative easing, to the benefit of emerging markets like India. This is a short-term hope, and will bring us right back to our structural problems.

- Replicate the policies of our own Indian states like Orissa and Chhattisgarh, whose finance ministers have focused on increasing revenues, lowering deficits and debt ratios and tackling issues of corruption.

- Pray for early elections, which will bring in a new team, hopefully one with conviction, some integrity and a better grasp of reality.

Manjeet Kripalani is the Co-founder and Executive Director of Gateway House: Indian Council on Global Relations.

This article was exclusively written for Gateway House: Indian Council on Global Relations. You can read more exclusive content here.

For interview requests with the author, or for permission to republish, please contact outreach@gatewayhouse.in.

© Copyright 2013 Gateway House: Indian Council on Global Relations. All rights reserved. Any unauthorized copying or reproduction is strictly prohibited.