The 2017 Spring International Monetary Fund (IMF) and World Bank meetings begin later this week. Despite the tide of populism and geopolitical uncertainties, the global economic recovery is gaining traction. Have we reached a turning point? And are global reform commitments needed to sustain the recovery?

The short answer to both questions is yes and yes. The growth outturns in the second half of last year have generally strengthened in the first quarter. Market sentiment has been rising, manufacturing and confidence indicators have picked up, and global trade volumes and commodity prices are rising. The world is clearly witnessing a strong cyclical recovery in investment, manufacturing, and trade. The IMF is likely to project a pickup in global growth this year and next—closer to 4%—compared to just over 3% in 2016.

Global conditions appear to be strongly driven by the U.S., helped by expectations of a more expansionary U.S. fiscal policy, corporate tax reform, and regulatory easing. This sentiment has lifted U.S. financial markets, and is correlating strongly with global financial conditions. Although retail sales fell again in March, and the March job report was weaker than the previous two months,[1] the underlying indicators signal that the U.S. labour market remains strong: the unemployment rate has fallen to 4.5%, the lowest level in almost a decade, and wages have risen. As such, the Federal Reserve is openly looking to raise rates multiple times over the next year and begin shrinking its balance sheet—moves that are likely to further strengthen the dollar.

The projected pickup in advanced economic activity is broader, helped by spillovers from the U.S. Economic activity is increasing beyond expectations in the Eurozone area, and also in the United Kingdom, and Japan. The Eurozone is enjoying its strongest expansion in several years. Japan is experiencing an acceleration of growth to a 19-month high, according to the Nikkei Purchasing Managers Index (PMI) surveys, buoyed by faster service sector activity as well as an export-related boost to manufacturing.

Emerging and developing economies, led by China and India, have also rallied, and should contribute three-quarters of total global GDP growth in 2017. The Emerging Market PMI reached a 31-month high in March.[2]India remains the fastest growing major country, concerns of China’s capital outflows and reserves have eased as its growth has stabilised, and commodity-exporting countries have been helped by their terms of trade. Despite prospects that the Federal Reserve will continue to tighten, investor interest in emerging markets surged this past quarter, and spreads for corporate bonds are hitting new lows—testimony to record bond issuance. As a result, stocks and currencies have rallied in India and many emerging markets.

Underlying fundamentals

Thus, the global economy is moving into a better position. But the underlying fundamentals are still weak in the advanced countries and in many emerging markets, and there are considerable risks to the outlook. The challenge for economic policy makers is to recognise these continuing challenges, and to take political advantage of cyclically improving economies to address the fundamentals with global consensus and multilateral actions.

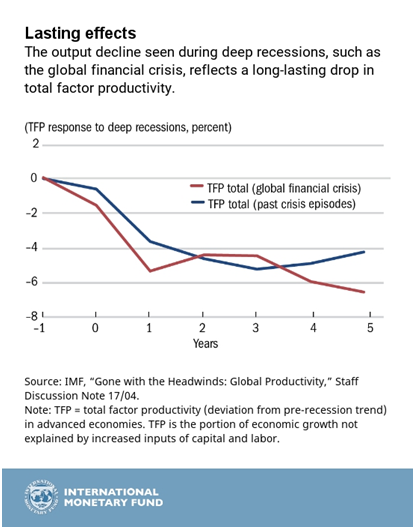

The fundamental global weakness is the sharp slowdown in measured output per worker and total factor productivity (TFP), despite rising technological innovation–and this has been well documented, including by the IMF.[3]The drop in TFP growth following the global financial crisis has been widespread and persistent, with recovery much slower than from previous financial crises (Chart).

Even before the global financial crisis, productivity growth was slowing in the U.S. and many other advanced countries. There was an abrupt further slowdown in advanced economies after the crisis, especially in the United Kingdom and Europe.[4] [5] Recent data on weak wages and low productivity in the United Kingdom exemplify the continuing challenge. This trend has also affected many emerging and developing countries, especially China, where productivity had been growing before the crisis. Among the contributory factors has been the slowdown of educational attainment in many countries that has led to declines in the labour share of income and consequent rising inequalities, especially in countries where technological progress has been most advanced. India’s productivity growth has been relatively less affected so far due to its reliance on services, but its reform agenda needs to intensify to forestall a slowdown.

Policy priorities

The challenges require near term actions and longer term structural reforms. In the near term, addressing legacy issues from the financial crisis is a clear imperative to begin reversing the decline in productivity growth. This is particularly the case in Europe, where financial and corporate restructuring is incomplete, and balance sheets are still not supportive of new corporate investment. Similarly, reining in leverage, and building the resilience of banks and corporations is also a challenge in many emerging countries, such as China and India, where the corporate sector remains over-indebted, detracting from new investments.

In the longer term, the global challenge is to induce greater risk-taking private investment in new areas that will lift productivity and potential growth, while also addressing rising inequalities. This will require a global consensus to reduce policy uncertainty and give clear signals about future economic policy, as the G20 has emphasised. The public policy agenda will need to build investment in high-return infrastructure, especially in education and training in new areas of technology and innovation, and tax incentives to raise investment in research and development.

Some enabling efforts are being made. In the United States, the administration is moving ahead to reduce corporate taxes, in line with other advanced countries, and simplify financial regulation but, importantly, without weakening its risk effectiveness. Structural reforms to deregulate product and labour markets, especially in services, is a priority across many advanced countries and emerging markets that needs to be reaffirmed.

Global commitments are critical to the process of unleashing new risk-taking investments. Among these, the historical evidence is clear that trade is an engine of growth and has delivered sizeable TFP gains in the past, and these must intensify, especially in new areas of services, technology, and investment. At the same time, attention needs to be given to strengthening education and training policies, through targeted education programmes and skills training, for example, that will better equip lower-skilled workers with the tools they need for better-paying jobs. These commitments are needed to build expectations of a more optimistic future that can then fuel higher demand, and spur new investment.

Without them, the risk of another decade of weak productivity growth looms, spawning populist policies that will impede trade and capital flows and dampen market sentiment. These negative spillovers will exacerbate existing corporate sector vulnerabilities, especially in emerging markets, and increase banking sector risks globally. It is reassuring that, at their recent meeting in Washington, Presidents Trump and Xi committed to developing a 100-day plan for greater trade and investment opening between the U.S. and China, moving away from concerns of a retreat from trade.

Anoop Singh is Distinguished Fellow, Geoeconomics Studies at Gateway House: Indian Council on Global Relations.

This article was exclusively written for Gateway House: Indian Council on Global Relations. You can read more exclusive content here.

For interview requests with the author, or for permission to republish, please contact outreach@gatewayhouse.in.

© Copyright 2017 Gateway House: Indian Council on Global Relations. All rights reserved. Any unauthorized copying or reproduction is strictly prohibited

References

[1] The jobs report on April 7 showed the economy added about 98,000 jobs in March, following increases of over 200,000 in January-February.

[2] “Global PMI data for March rounds off best quarter for two years”, IHS Markit, April 7, 2017, <http://www.markit.com/Commentary/Get/07042017-Economics-Global-PMI-data-for-March-rounds-off-best-quarter-for-two-years?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+MarkitPMIsAndEconomicData+%28Markit+PMIs+and+Economic+Data%29>

[3] IMF Blog: Insights and Analysis on Economics and Finance, IMF, Chart of the Week: Slow Productivity: Why It Matters and What To Do, April 3, 2017, <https://blog-imfdirect.imf.org/2017/04/03/chart-of-the-week-slowing-productivity-why-it-matters-and-what-to-do/>;

IMF Staff Discussion Note, IMF, Gone with the headwinds: Global Productivity, by Gustavo Adler, Romain Duval, Davide Furceri, Sinem Kiliç Çelik, Ksenia Koloskova, and Marcos Poplawski-Ribeiro, April 2017, <http://www.imf.org/en/Publications/Staff-Discussion-Notes/Issues/2017/04/03/Gone-with-the-Headwinds-Global-Productivity-44758>

[4] Bank of England, Productivity puzzles, Speech given by Andrew G. Haldane, March 20, 2017, <http://www.bankofengland.co.uk/publications/Documents/speeches/2017/speech968.pdf>

[5] IMF, Speech: Reinvigorating Productivity Growth, Speech given by Christine Lagarde, April 3, 2017, <http://www.imf.org/en/news/articles/2017/04/03/sp040317-reinvigorating-productivity-growth>