The following is an extract from an essay on Latin America’s experience with conditional cash transfers and the lessons that can be derived for India. You can read the full essay here.

The past decade has seen numerous innovations in social policy, which go beyond previous approaches like subsidies and non-monetary provisions. One of the most popular incentive-based social innovations has come from Latin America, in the form of conditional cash transfers (CCTs).

This new tool of social equity has found success in a number of Latin American countries, where governments transfer cash grants to the poor upon meeting conditions that usually focus on education, and child and maternal health.

The rapid spread of CCT programmes in Latin America over the past decade, to practically every country in the region—except Cuba and Venezuela—has strengthened the argument for targeted social programmes, and it raises new questions related to the evolution and efficiency of such programmes: why has Latin America, unlike other regions, responded so positively and quickly to implement CCTs? What can we learn from the diverse Latin American experience with CCTs?

In attempting to answer such questions, we must be cautious in arriving at conclusions which may generalise outcomes rather than provide genuine insight into particular programmes. It is difficult to determine the extent of the impact that CCTs can have on the poor, and whether such impact can be reflected in measurements of poverty and other social indicators. The results will also vary depending on the country, the scale and nature of CCT programmes in place.

The CCT programmes in Brazil and Mexico—currently the longest continuously running CCT programmes in the world at the moment—have been through empirical analysis and randomised control trials for two decades. This great body of evidence shows that such programmes can have positive effects. In a 2009 World Bank Policy Report, Ariel Fiszbein and Norbert Schady note that “what really makes Mexico’s programme iconic are the successive waves of data collected to evaluate its impact, the placement of those data in the public domain, and the resulting hundreds of papers and thousands of references that such dissemination has generated.”[1]

But there have also been criticisms against CCTs: some suggest unconditional cash transfers (UCTs) as an alternative, or that governments should instead prioritise broader developmental issues like potable water, basic infrastructure, and healthcare. There have also been allegations of clientelism and reports of severe leakages, which have been attributed to corrupt officials and an opaque delivery system.

Overall, there is a sense that, if CCTs are conceived and executed properly, they can bring about swift and positive results, especially in the areas of school enrolment, child and maternal health. In principle, CCTs are only temporary solutions, and the government’s focus must remain on building the capacity and quality of state institutions.

CCTs in India: Feasibility

Conditional cash transfer programmes have operated in small numbers in countries like Costa Rica, with 190,000 beneficiaries, and in large numbers in countries like Brazil, with 52 million beneficiaries. They have been tested and revised regularly to improve targeting, and reduce leakages and structural inequities.

The Latin American experience with CCTs is proof that they can work if implemented well, but would such programmes be feasible for a country of 1.2 billion people like India, where two-thirds of the total population lives in rural areas with poor connectivity?[2] There are 363 million people in India living below the poverty line,[3] and 260 million of them live in rural areas. The main obstacles for CCTs in India would be those related to access, identification, classification, monitoring and evaluation of poor households. A number of structural questions must also be answered: should CCT programmes be driven from the top-down or started first in smaller municipalities and then scaled up? What conditions should be imposed on the beneficiaries, and how will these be enforced?

Background of existing social programmes in India

National Rural Employment Guarantee Scheme (NREGS): India has more than 200 active social programmes in its 29 states and seven union territories. The biggest programme, the National Rural Employment Guarantee Scheme (NREGS) guarantees each rural household 100 days of wage employment (to do unskilled manual work) each year; unlike the CCTs in Latin America, the NREGS places little or no conditions. Although the implementation of the NREGS has been shaky, with numerous allegations of corruption, its scale is unprecedented. According to a 2014 study, it is “the largest workfare programme globally, covering 11% of the world’s population. The Government of India’s allocation to it for fiscal year April 2013-March 2014 was Rs.330 billion (US $5.5 billion), or 7.9% of its budget.”[4]

Janani Suraksha Yojana (JSY): Launched in 2005 under the National Rural Health Mission, JSY seeks to “reduce maternal and neo-natal mortality by promoting institutional delivery, i.e. by providing a cash incentive to mothers who deliver their babies in a health facility.”[5] It is a nation-wide programme, which provides a cash benefit of Rs.1,400 (in rural areas) or Rs.1,000 (in urban areas) to women below the national poverty live who give birth in government-affiliated health facilities.[6] An important feature of this scheme is the role of the Accredited Social Health Activist, or ASHA, who is responsible for a multitude of tasks: to identify and register beneficiaries, assist women in receiving health check-ups, identifying a government health facility for delivery, escorting pregnant women to health centres, arranging vaccines for the child, postnatal visits within one week of safe delivery, and finally, to counsel matters related to breastfeeding and family planning. For all their assistance, the ASHA is paid a nominal package of Rs.600 (in rural areas) or Rs.200 (in urban areas).

While most evaluations find that the number of births in health facilities have increased, the impact of JSY on maternal and infant mortality is difficult to determine. But there remain a number of challenges related to the implementation of the program. Notably, a 2009 UNFPA study concluded that while the findings indicate “a huge increase in institutional deliveries in the low performing states,” the administration must utilise spare capacity in the private sector to provide institutional health services.[7] Due to irregular payments to the ASHAs in some states like Bihar where only 20.7% receive regular payment, the study adds that “grievance cells should also be set up to look into the complaints related to non-payment of ASHAs.”

Challenges to CCTs in India

Given the sheer scale of India’s poor and vulnerable population, and the large array of tasks to be completed if and when India implements cash transfers on a national scale, there are bound to be numerous challenges. One of the main complications confronting India is the lack of access to its poor through a national identification database (though one such database, the Aadhar, is currently being built). The poor themselves lack access to affordable and quality healthcare. An article in the PLOS Medicine journal states that “due to chronic low government expenditure on health care, there is only one primary health centre (PHC) for 34,641 people, one government doctor for about 20,000 rural population and most public health facilities do not have adequate medicines.”[8] Furthermore, a large number of the poor in India are not linked to financial institutions. According to a 2012 World Bank study, only 35% of adults in India have an account with a formal financial institution.[9]

Two Indian scholars at the Harvard Kennedy School, Kartik Akileswaran and Arvind Nair, stress that the Indian state is not ready for the switch to cash. Their argument is based on two primary rationalisations: first, India requires “significant additional capability in identifying households and in linking households to bank accounts” and secondly, the “increase in economic welfare will only be realised if the cash transfer is equivalent in purchasing power to the subsidy.” The authors also believe that the government’s implementation strategy lacks the ability to adapt to the above-stated shortfalls; their only suggestion, which remains sound, is that India should “emulate the successful bottom-up implementation approach of Brazil’s [Bolsa] Família with gradual scale up from the regional to the national level.”[10]

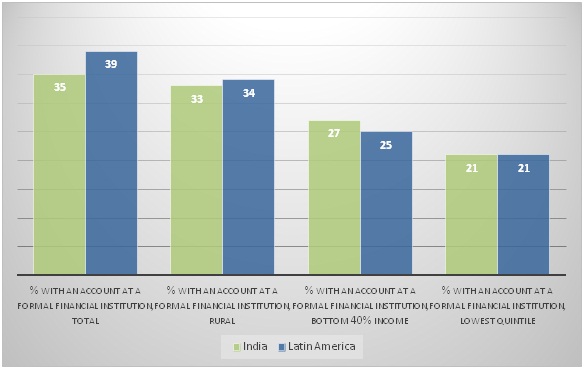

Surprisingly, however, even though the authors stress India’s lack of financial inclusion as an impediment for CCT programmes, India’s financial inclusion data is not very different from Latin America, which has successfully implemented CCTs. Of the bottom 40% of the population by income in India, 27% have a bank account, which is higher than the share of the bottom 40% of the population in Latin America with a bank account at 25%.[11] In both India and Latin America, 21% of the bottom income quintile have a bank account; and 34% of those in rural Latin America have a bank account, compared with 33% of those in rural. These statistics show that India and Latin America share a similar level of financial inclusion (see chart below).

Chart 1. Financial inclusion in India & Latin America (source: Financial inclusion data, World Bank)

A three-pronged solution

In India, where problems abound, the real demand is for pragmatic solutions. The government’s decision to go ahead with the social assistance through subsidies i.e. Direct Benefit Transfer (DBT) has to be seen in this context; it is a plea to reduce the level of corruption by removing middlemen and initiating a more transparent system. Three broad solutions, or ideas, could help minimise the government’s obstacles and make the transition to DBTs easier:

- In December 2012, Dr. Sameer Sharma, a member of the Indian Administrative Service, suggested that cash transfers should be a “mix of categories, for example, paying Rs.500 to all the poor, and conditional transfer, say, another Rs.300 for children regularly attending school.” He adds that “to minimise risk of spending disproportionately on things like liquor, conditional cash transfer has to complement direct transfers. Conditional transfers will take care of specific policy objectives, say, of poverty reduction, developing markets, removing social and economic discrimination.”[12]

- While it is true that only roughly one-third of Indians have a bank account, we must keep in mind that 886 million Indians (71% of the population) have mobile phone connections.[13] This vast network can be leveraged through innovative mobile banking models—where money is transferred directly to mobile phones in case the beneficiary does not have a bank account. Sharma suggests that another innovation “could be to verify the Aadhaar identity using the camera of the mobile phones.” India can learn from the positive experience of African countries like Kenya and Tanzania, where the total value of transactions made in 2013 through mobile money constituted more than 50% of the countries’ GDP.[14]

- In the case of CCTs, while lack of sufficient public healthcare services is an impediment, the role of private healthcare can be seen as an opportunity. India’s private healthcare industry holds itself to global standards in many respects, and a number of foreign patients choose India as their destination for low-cost, high-quality healthcare services. In conjunction with the private sector, the government could work towards increasing access to healthcare in rural areas and integrate social assistance programmes with private health facilities.

Conclusion

The success of CCT programmes in Latin America have been highlighted in numerous studies over the past few years, not only by scholars in academia, but also by government technocrats and financial institutions like the IDB and World Bank, which have played a role in the evolution of CCTs in Latin America. There are some lessons we can take from these analyses.

Although CCTs have been championed by Latin America, we must keep in mind that instead of replicating the same models, countries must devise one suited to their own socio-economic environments. For instance, the Indian government may not be able to place similar conditions of regular health checkups or 80%-90% school attendance in rural areas where health facilities are scarce or at times don’t even exist, or in rural government schools where teachers are often absent due to insufficient pay.

The lesson then is to customise CCTs, and after launching them in pilot schemes, scale up from the bottom. The leakages from CCTs can also be fixed by making systems more transparent and tracking payments electronically. The experience of Mexico, which has switched fully from cash to electronic transfers since 2011, has taught us that electronic transfers can be cost-effective, more transparent, quicker, and also increase financial inclusion. After all, CCTs are not a cure-all for poverty alleviation, and the focus for India will remain on development issues related to infrastructure and connectivity, provision of public goods and services especially to those in the rural areas, the creation of more jobs and economic growth.

Hari Seshasayee is a former researcher with Gateway House: Indian Council on Global Relations. He is currently pursuing a Masters in Latin American Studies at Stanford University.

This article is an extract from an essay. You can read the full essay here.

For interview requests with the author, or for permission to republish, please contact outreach@gatewayhouse.in.

© Copyright 2015 Gateway House: Indian Council on Global Relations. All rights reserved. Any unauthorized copying or reproduction is strictly prohibited.

References

[1] Fiszbein, Ariel and Norbert Schady, ‘Conditional cash transfers: reducing present and future poverty’, World Bank, 2009 <http://econ.worldbank.org/WBSITE/EXTERNAL/EXTDEC/EXTRESEARCH/

0,,contentMDK:23027684~menuPK:574960~pagePK:64165401~piPK:64165026~

theSitePK:469382~is

CURL:Y~isCURL:Y,00.html> pp 6

[2] Central Intelligence Agency, World Factbook-India, <https://www.cia.gov/library/publications/the-world-factbook/geos/in.html>

[3] Planning Commission, Report of the Expert Group to Review the Methodology for Measurement of Poverty, June 2014, <http://www.indiaenvironmentportal.org.in/files/file/Rangarajan%20poverty%20

report.pdf> pp 5

[4] Muralidharan, Karthik, Paul Niehaus, and Sandip Sukhtankar, ‘Building State Capacity: Evidence from Biometric Smartcards in India’, National Bureau of Economic Research, March 2014 < http://www.nber.org/papers/w19999.pdf>

[5] UNFPA, India-Concurrent assessment of Janani Suraksha Yojana (JSY) in selected states, 2009 < http://countryoffice.unfpa.org/india/drive/JSYConcurrentAssessment.pdf>

[6] National Rural Health Mission, Health & Family Welfare Department, Operational guidelines for implementation of janani suraksha yojana, Government of Orissa <http://angul.nic.in/jsy.pdf>

[7] UNFPA, India-Concurrent assessment of Janani Suraksha Yojana (JSY) in selected states, 2009 < http://countryoffice.unfpa.org/india/drive/JSYConcurrentAssessment.pdf>

[8] Devadasan, Narayanan, Soumitra Ghosh, Sunil Nandraj and T. Sundararaman, ‘Monitoring and evaluating progress towards universal health coverage in India’, PLoS medicine, 22 September 2014 <http://www.plosmedicine.org/article/info%3Adoi%2F10.1371%2Fjournal.pmed.

1001697>

[9] World Bank, Financial Inclusion Data-India <http://datatopics.worldbank.org/financialinclusion/country/india>

[10] Nair, Arvind, and Kartik Akileswaran, ‘India’s cash transfer model: a rushed and flawed welfare scheme?’, The Guardian, 19 August, 2013 <http://www.theguardian.com/global-development-professionals-network/2013/aug/19/india-cash-transfer-welfare>

[11] World Bank, Latin America and Caribbean-Financial Inclusion Data, <http://datatopics.worldbank.org/financialinclusion/region/latin-america-and-caribbean>

[12] Sharma, Sameer, ‘Direct Cash Transfer scheme: India must learn from Latin America and Kenya’, The Economic Times, 12 December 2012 <http://articles.economictimes.indiatimes.com/2012-12-12/news/35773812_1_direct-cash-transfer-conditional-cash-poor-families>

[13] International Telecommunication Union, Mobile-cellular subscriptions, <http://www.itu.int/en/ITU-D/Statistics/Documents/statistics/2014/Mobile_cellular_2000-2013.xls>

[14] The Economist, Mobile money in developing countries, 20 September 2014 <http://www.economist.com/news/economic-and-financial-indicators/21618842-mobile-money-developing-countries>